Companies featured here may provide compensation for click throughs. This is how I maintain free research for consumers. My full disclosure of who I invested with is on this page for transparency.

An Individual Retirement Account, commonly referred to as an IRA, is a retirement savings vehicle designed to offer tax benefits. Contributions to a Roth IRA require you to pay income taxes upfront, but offer tax-free withdrawals in retirement. When you invest money into this account, your contributions may qualify for immediate tax advantages or provide future tax benefits upon withdrawal during retirement. This article aims to demystify the workings of IRA accounts by discussing their operation and detailing the varieties at your disposal, thereby assisting in selecting the most suitable one that aligns with your financial aspirations for retirement.

Individual Retirement Account Things to Know

- An Individual Retirement Account (IRA) is a tax-advantaged investment account available to anyone with earned income, designed to help individuals save for retirement with the benefits of tax-deferred or tax-free growth.

- There are several types of IRAs including Traditional, Roth, SEP, and SIMPLE IRAs, each offering unique benefits and tax advantages tailored to different financial situations and retirement planning needs.

- IRA contributions are subject to annual limits ($7,000 for individuals under 50 and $8,000 for those 50 or older in 2024), and understanding the tax implications and withdrawal rules for each type of IRA is crucial for maximizing retirement savings and avoiding penalties.

A retirement account known as an Individual Retirement Account (IRA) represents a beacon of financial security for those planning for their golden years. This tax-advantaged investment account is specifically designed to aid individuals who are focused on setting themselves up financially for the future. The acronym IRA stands not only for “Individual Retirement Account” but also for “Individual Promotion and Marketing Standing,” emphasising its personal nature and potential impact on post-career life savings. In contrast to 401(k) plans that are often employer-associated, individual retirement accounts offer anyone with earned income a private and adaptable avenue to accumulate retirement funds.

The compelling attraction of IRAs revolves around the substantial tax benefits they provide. Many choose to open an IRA due to its ability to cultivate one’s retirement reserves through either tax-deferred or completely tax-free growth methods – this pivotally allows investors foresight in knowing they can foster their nest egg while enjoying advantageous taxation circumstances. Simplifying matters, establishing an IRA can be done effortlessly since banks, brokerage firms, and other financial institutions readily make these accounts available.

IRAs serve as a crucial foundation within the realm of retiree strategic preparation, regardless of whether you’re navigating self-employment waters, operating your own business entity or pursuing additional avenues alongside your current provisions.

What Is an IRA?

Definition of an IRA

An Individual Retirement Account (IRA) is a tax-advantaged investment account designed to help individuals save for retirement. By allowing you to contribute a portion of your income to a retirement account, an IRA provides a structured way to grow your savings either tax-deferred or tax-free, depending on the type of IRA you choose. This makes IRAs one of the most effective tools for long-term financial planning. The tax benefits associated with IRAs can significantly enhance your retirement savings, offering you the flexibility to invest in a variety of assets such as stocks, bonds, mutual funds, and exchange-traded funds (ETFs). Whether you opt for a traditional IRA or a Roth IRA, these accounts are designed to help you build a robust financial foundation for your retirement years.

How Does an IRA Work?

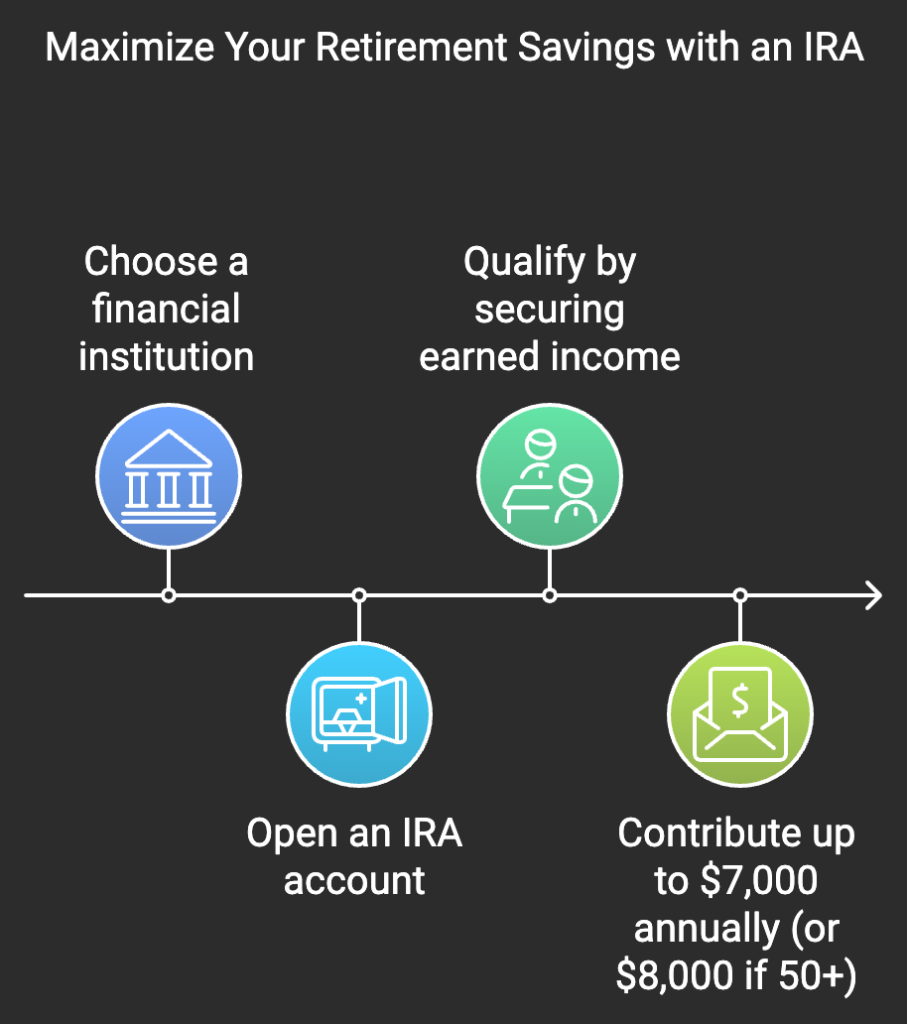

When you opt to steer your retirement savings through an IRA, the first step is to select a financial institution that fits your needs. This could be anything from a conventional bank to an innovative robo-advisor – all offering the option to open an IRA account. Once you qualify, mainly by securing earned income, you’re entitled to pump in up to $7,000 for 2024 or $8,000 if age 50 and above into this investment vehicle annually. Your money can then be allocated across various investment opportunities such as:

- Stocks

- Bonds

- Mutual funds

- Exchange traded funds (ETFs)

The enchantment of an IRA springs from its capacity for tax-deferred growth, which allows the investments within your account to compound more efficiently by postponing taxes on gains. Those who favor hands-on management with IRAs have even greater flexibility. Beyond mainstream securities like stocks or bonds, they might venture into alternative assets including real estate ventures, precious metals or cryptocurrency markets – expanding their personal portfolio landscape extensively. Having a workplace retirement plan like a 401(k) doesn’t exclude participation in an IRA, but rather complements it. IRAs can be used alongside an employer-sponsored plan to enhance retirement savings by providing additional investment options and tax advantages.

Types of IRAs

The array of IRAs available is extensive and diverse, accommodating the retirement planning needs of individuals from various walks of life. Whether one is a freelance professional, runs their own small business, or wishes to dive into the innovative territory of cryptocurrency investments, there exists an IRA suitable for every scenario. The most well-known variants include:

- Traditional IRA

- Roth IRA

- SEP (Simplified Employee Pension) IRA

- SIMPLE (Savings Incentive Match Plan for Employees) IRA

Each variant presents distinct features and advantages specifically designed to align with different financial circumstances.

Additional types of IRAs broaden this spectrum even further. These encompass specialized accounts like Bitcoin IRAs, inherited IRAs, and spousalIRAS enriching the variety of choices at disposal, to ensure that individuals can secure an optimal match for their retirement saving approach.

Traditional IRA

A Traditional IRA stands as a crucial tool for those charting their retirement savings path, offering immediate tax relief advantages. By making tax deductible contributions to this account, you have the opportunity to lower your taxable income in the present while deferring taxes until withdrawals during retirement. This option is attractive especially for individuals who expect to be in a lower tax bracket upon retiring, thus potentially paying less taxes on their nest egg when that time comes. Additionally, while contributions may be tax-deductible, you will need to pay taxes on withdrawals during retirement.

It should be noted though not every contribution made into a Traditional can indeed qualify as non-deductible. These allow greater versatility for contributors who do not fulfill requirements necessary for upfront deductions.

In essence, the Traditional IRA represents an optimal strategy for savers seeking up-front deduction benefits from their taxable income and are amenable to deferring payment of taxes until post-retirement—a period when they might benefit from being in a reduced tax bracket.

Roth IRA

With a Roth IRA, you settle your tax obligations upfront by paying taxes on the money you put in, thereby securing entirely tax-free withdrawals under specific qualifying conditions. This appeals to those who believe they may be subject to a higher tax bracket upon retirement because it ensures them an income that is not taxed during their later years. The absence of age limits for contributions—as long as there’s earned income— combined with the capability to pull out what you’ve contributed without facing taxes or penalties after five years and once 59.5 has been reached, establishes the Roth IRA as both adaptable and potent for orchestrating one’s financial future.

The exemption from required minimum distributions (RMDs) stands out among the key benefits of utilizing a Roth IRA. This means your savings have more time to expand without being diminished by taxes. Although contribution capabilities can be influenced by how much one earns—with upper-income individuals potentially phased out—the technique known as backdoor Roth conversions provides even high earners access to Roth accounts. Those who prioritize having untaxed earnings grow over time—and are inclined toward handling their taxable liabilities presently in preparation for unrestricted access later—find great value in employing a Roth IRA strategy.

SEP IRA

The SEP IRA, short for Simplified Employee Pension Individual Retirement Account, serves as a boon for small business owners and self-employed individuals by offering them an opportunity to save for retirement with higher limits on contributions and less administrative hassle. Small businesses benefit from these plans as they can make substantial employer-funded contributions towards the employee’s retirement fund—ideal for businesses with fewer employees. Self-employed individuals find in the SEP IRA an equivalent to larger corporate pension benefits without having to navigate through complex regulations.

Although primarily designed around employers’ ability to contribute, it is ultimately advantageous for employees who receive added funds toward their retirement savings without being required to contribute themselves. This setup positions the SEP IRA as an excellent option not only for business proprietors but also independent professionals seeking a simple method of building up retirement assets both for them and their workforce. Thereby promoting a culture focused on long-term savings and financial wellbeing.

SIMPLE IRA

Designed specifically for small business owners, the SIMPLE IRA—short for Savings Incentive Match Plan for Employees—is an uncomplicated retirement plan that’s easy to implement and manage, even if the company has never offered a retirement plan before. It empowers employees to contribute a portion of their salary towards retirement savings while also receiving employer contributions. These can be consistent at 2% of employee pay or as much as a matching contribution up to 3%. Such structure provides motivation for both parties: employers get a straightforward way to contribute, and employees are incentivized to save.

Ideal for smaller companies looking for an economical method to support their workforce in building nest eggs with beneficial tax implications, the SIMPLE IRA offers simplicity and cost-efficiency. Both workers and employers benefit from its transparent system that simplifies setting aside money toward retirement savings. Companies focusing on moderate-sized payroll find it especially fitting due to its capacity not only bolstering staff members’ financial security into old age, but also providing enticing tax advantages.

Gold IRA

A gold IRA allows you to invest in precious metals within your IRA. This type of account acts as a safeguard against economic uncertainty, inflation, and global tensions. When markets suffer a downturn, precious metals tend to thrive. This provides a balanced investment safeguarding against the unknowns, such as a sudden stock market crash. It’s a strategy I personally invested in and highly believe in. You can learn more about gold IRAs on this page.

>> Get a Free Gold IRA Guide from the Company I Personally Used here >>

Eligibility and Contributions

Eligibility

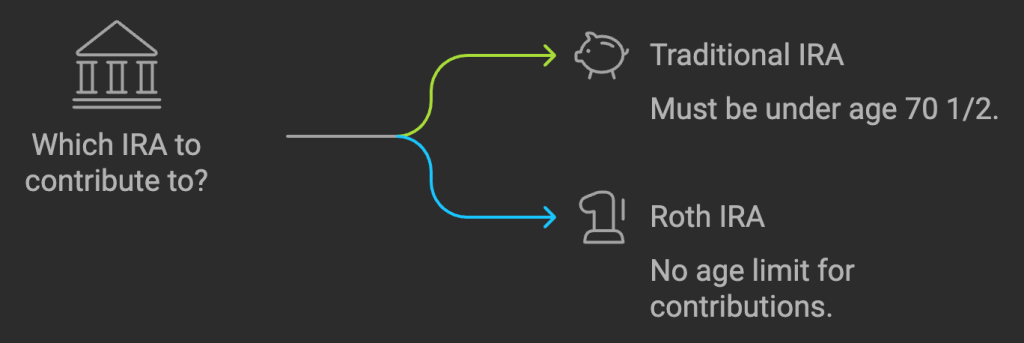

To contribute to an IRA, you must have earned income, which includes wages, salaries, and tips. For traditional IRAs, you must be under the age of 70 1/2, while Roth IRAs have no age limit for contributions. Additionally, your income must fall below certain thresholds to qualify for tax-deductible contributions. This means that even if you have a high income, you can still contribute to an IRA, but the tax benefits may vary. Understanding these eligibility criteria is crucial for maximizing the tax advantages and ensuring that your retirement savings strategy aligns with your financial goals.

IRA Contribution Limits

To effectively steer through the realm of IRA contributions, it is essential to be cognizant of the contribution limits set annually. In 2024, individuals who are under the age of 50 can invest up to $7,000 across all their personal IRAs collectively. For those aged 50 and above, an additional catch-up provision allows for a grand total contribution of $8,000. These ceilings encompass any number of IRA accounts you may own. Thus your combined deposits should not exceed these totals.

Adherence to these caps ensures that your retirement savings chart a prudent course while capitalizing on the tax benefits linked with IRA accounts.

Traditional IRA Contribution Limits

Contributions to Traditional IRAs may be tax-deductible, but this benefit depends on your income level and whether you or your spouse participate in a retirement plan at work. For the 2024 tax year, single individuals enrolled in an employer-sponsored retirement plan can deduct their entire IRA contributions if they earn $77,000 or less as MAGI. Married couples who file jointly are allowed a higher threshold of $123,000 for full deduction benefits.

Should your earnings exceed these specified limits while still necessitating payment of income taxes, partial deductions could still apply to your situation. It’s different for married persons filing separately. Here the range phases out quickly with MAGI needing to stay below $10,000 for any potential deduction.

Grasping these limitations concerning the contribution and its deductible nature is critical when trying to optimize Traditional IRA benefits—particularly when managing joint finances within dual-income families or if included under an employment-related retirement strategy.

Roth IRA Contribution Limits

Roth IRAs offer the advantage of tax-free income during retirement, but they come with restrictions on how much you can contribute based on your Modified Adjusted Gross Income (MAGI). As MAGI increases, contributions to Roth IRAs may be phased out. In 2024, individuals who file as single will see this phase-out start at an MAGI of $146,000 and end at $161,000. For married couples filing together, it begins at a combined MAGI of $230,000 and ends at $240,000. Should your earnings exceed these upper thresholds, you will not have the ability to directly put money into a Roth IRA.

When considering retirement savings strategies within the framework of constantly evolving tax regulations and financial goals, high earners should pay particular attention to their income levels relative to the limits set forth for Roth IRA contributions. Those whose incomes exceed these limitations might need alternative methods such as backdoor Roth IRAs in order to benefit from what traditional Roth IRAs have to offer. Keeping up-to-date with these income brackets is crucial for aligning your approach towards accumulating retirement funds with fiscal objectives.

Tax Benefits of IRAs

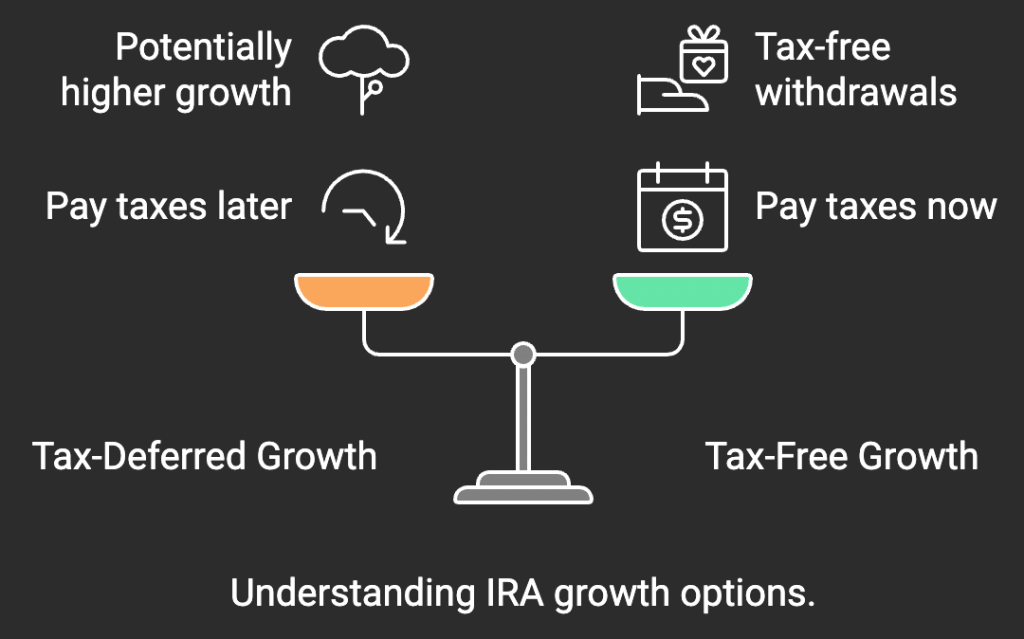

Investing in an IRA offers a variety of tax advantages, which differ based on the type you select. Whether it’s a Traditional or Roth IRA, both are structured to reduce your overall tax burden. Contributions made to a Traditional IRA might qualify for deductions from your taxable income, thereby lowering your immediate tax bill while adding to the account. Any growth within your Traditional IR accounts is taxed only at the time withdrawals begin.

Conversely, with contributions composed of after-tax dollars that aren’t deductible upfront, Roth IRAs offer distinct fiscal perks. The accumulation of assets inside these accounts occurs entirely free from taxes and qualified disbursements during retirement incur no Taxation either. This can prove exceptionally advantageous for individuals who predict they will fall into higher brackets as retirees or wish to decrease their future payable taxes considerably throughout retirement periods. With their potential impact on flourishing retirement savings markedly positive over time through compounding benefits—the strategic use of both traditional and Roth IRAs serves as key components in effective financial planning strategies aimed towards securing more comfortable retirements.

Flexibility of IRAs

IRAs offer remarkable flexibility in terms of investment options, allowing you to choose from a wide range of assets such as stocks, bonds, mutual funds, and exchange-traded funds (ETFs). Depending on your individual circumstances and financial goals, you can opt for a traditional IRA or a Roth IRA. Traditional IRAs provide the benefit of tax-deductible contributions, which can lower your taxable income in the present. On the other hand, Roth IRAs offer the advantage of tax-free growth and withdrawals, making them an attractive option for those who anticipate being in a higher tax bracket during retirement. Additionally, IRAs can serve as a valuable supplement to other retirement income sources, such as employer-sponsored plans, and can be used to save for various long-term goals, including education expenses. This flexibility makes IRAs a versatile and powerful tool in your retirement planning arsenal.

IRA Withdrawals

When nearing retirement, the emphasis transitions from adding to your IRA to taking distributions from it. Comprehending the regulations that apply to withdrawals is crucial, similar to how vital it was understanding contribution rules. With both Traditional and Roth IRas, once you reach 5912 years old, you’re typically allowed penalty-free access. While traditional IRA distributions count as taxable income at that point, Roth IRAs provide tax-free withdrawals under specific conditions. Premature tapping into retirement savings before this milestone could activate a 10% early withdrawal penalty on top of any applicable taxes—this can substantially diminish the value of your accumulated retirement funds.

Early Withdrawals

At times, unforeseen circumstances may necessitate dipping into your retirement savings sooner than you anticipated. In such events, if funds are taken out from an IRA before reaching 5912 years of age, there is usually a penalty fee of 10% that applies. To the standard income taxes on the amount withdrawn. It’s important not to lose hope. Exceptions for waiving this early withdrawal penalty do exist and are sanctioned by the IRS under certain qualifying situations which include:

- Covering medical expenses

- Funding higher education pursuits

- Investing in a first home

- Paying insurance premiums following loss of employment

Those who have invested in a Roth IRA benefit from additional flexibility when facing financial challenges. Contributions made towards a Roth-K can be retrieved at any point without attracting penalties or tax implications. This leniency does not extend to earnings generated from those contributions. Awareness of these specific regulations and exemptions is essential both for safeguarding against potential fiscal shocks and preserving the intended purpose of your retirement funds.

Choosing the Right IRA for Your Financial Situation

Choosing between a Traditional IRA and a Roth IRA should be based on your current financial status, anticipated future tax rates, and specific retirement objectives. Opt for a Traditional IRA if you’re currently in the upper tax brackets but anticipate dropping to lower ones post retirement. This choice provides immediate tax breaks with taxable withdrawals in the future. If you see yourself being taxed at higher rates when you retire or value having access to funds that won’t be taxed later, then selecting a Roth 401(k) could serve you better.

A financial advisor can offer customized guidance regarding which type of IRA—traditional or Roth—is most compatible with your economic plans. With their expertise, they’ll assist you in understanding intricate aspects of taxation rules, contribution limits pertaining to each option along with suggesting appropriate investment tactics that cater specifically to your distinct needs and aspirations related to retirement savings.

How to Open an IRA

Setting out to open an IRA is essentially laying the groundwork for a solid financial future. Firstly, confirm your eligibility by having earned income or a taxpayer identification number such as an SSN or TIN. Then choose a financial institution that matches your investment ethos and requirements, taking into account aspects such as service charges, customer support quality, and the diversity of investment opportunities they offer. Once these initial steps are taken care of, proceed with completing the required documents which include Form 5305-R for IRS submission and provide necessary details including ID verification, bank information, and beneficiary designations.

Don’t be intimidated by the process of opening an IRA. It can actually be quite straightforward whether you decide to go through your local banking establishment talk with a finance professional or even initiate the setup online via brokerage services. After establishing your account, not only will you have started saving but also investing toward long-term growth potential stability within Your Future Financial Landscape. Reviewing various funding options regularly is critical to ensuring staying in line with changing Retirement objectives personal fiscal circumstances.

Related Reading: Can I Contribute to an IRA After Retirement?

Rollover IRAs

Individuals in the midst of a job change or who wish to take more control over their retirement savings may find that transferring their funds into a Rollover IRA is an advantageous move. By moving money from an employer-sponsored account like a 401(k) into this type of individual retirement account, you can keep your assets’ tax-deferred status and avoid penalties usually associated with early withdrawals. A rollover could be beneficial if the investment options available through your previous employer’s plan are unsatisfactory, or if employment termination cuts off access to that plan.

To ensure the retention of your retirement savings’ tax advantages and steer clear of adverse tax consequences, it’s critical to carefully manage the transition process when contemplating a rolover. While there are multiple paths—including retaining funds within the old employer’s scheme, shifting them into a new employer’s program, or cashing out—the last option often triggers taxes plus additional fines immediately upon withdrawal. This makes initiating a rollover IRA frequently perceived as preferable for many individuals.

Opting for a Rollover IRA opens up broader investment opportunities while safeguarding chances for ongoing growth on a tax-deferred basis – thereby serving as an important strategy in adeptly stewarding one’s nest egg designated for later years.

Managing Your IRA Investments

Navigating the intricacies of IRA investment management involves striking a balance between your risk tolerance and a clear plan for your retirement years. This tolerance, influenced by how comfortable you are with market volatility and the remaining time until you retire, should direct where to place your funds—be it in mutual funds, ETFs or bonds. The composition of assets within your portfolio – covering stocks, bonds, and cash – is pivotal to finding an equilibrium that aligns with both your appetite for risk and the prospective rewards.

For investors aspiring toward portfolio diversification:

- A variety of instruments like mutual funds and exchange traded also known as ETFs offer access to numerous markets including reputable companies listed on indices such as S&P 500 along with international entities—all this without having to buy individual shares.

- Turning over investment decision-making to robo-advisors could streamline managing one’s investments. These digital platforms curate diversified portfolios reflective of an investor’s age alongside their tolerance for financial risk while charging nominal fees.

- Investors advancing towards retirement may find respite in target-date funds which autonomously modify asset allocation tailored closer when nearing those latter years thus methodically diminishing exposure levels tied into risks associated therein.

Required Minimum Distributions (RMDs)

As retirement approaches, it becomes increasingly vital to focus on the Required Minimum Distributions (RMDs) associated with Traditional IRAs. Once you reach 73 years old, you are obligated to start withdrawing these RMDs from your IRA and other eligible plans. The first withdrawal must occur by April 1 of the year following when you turn this age. To determine each distribution amount, divide your entire IRA balance by an IRS-provided life expectancy factor. This spreads out withdrawals across what remains of your lifespan.

Neglecting to withdraw the correct RMD can result in severe financial consequences. Any deficiency between the required and actual withdrawn amounts is subject to a significant tax penalty—initially set at 25%. Should one rectify their mistake promptly enough, that rate may be reduced down to 10%. While individuals have latitude in choosing whether they want their total annual RMD taken from just one or multiple IRAS,—note that for inherited accounts or specific qualifying pensions—it’s mandatory that separate calculations and distributions are executed for each plan.

To avoid any unnecessary fines while transitioning into retirement seamlessly, comprehensive knowledge about how RMDs function within personal pension planning is imperative.

The journey through the world of Individual Retirement Accounts is one that leads to a future of financial security and peace of mind. From understanding the tax-advantaged nature of IRAs to navigating the different types, contribution limits, and withdrawal rules, this guide has equipped you with the knowledge to make the most of these retirement savings vehicles. Whether you opt for the upfront tax deductions of a Traditional IRA or the tax-free growth of a Roth IRA, the importance of managing your investments and planning for RMDs cannot be overstated. As you reflect on the steps to open an IRA, consider rollovers, and manage your investments, remember that taking control of your retirement savings today is the surest way to enjoy a financially secure retirement tomorrow.